PREA Quarterly Spring 2025: Reframing Risk: A Data-Driven Case for Investing in Secondary and Tertiary Markets in the Western US

Originally posted in PREA Quarterly Spring 2025

by Jon Salzberg and Casey Kahler

Prevailing institutional groupthink has long preferred primary markets as the de facto target for core and value-added real estate strategies. However, nascent research suggests that secondary and tertiary markets in the Western US may offer not only competitive but in many cases superior economic stability and real estate performance. Drawing on two decades of comparative data across economic indicators and real estate fundamentals, this article presents a comprehensive reassessment of the investment potential in secondary and tertiary Western US markets. By analyzing long-run patterns in GDP growth, job creation, population trends, and commercial real estate metrics across multifamily and industrial sectors, we offer a robust, datadriven perspective on why these smaller markets merit institutional attention. As capital allocators face a structurally shifting landscape, rethinking geographic allocation could prove essential not just for alpha generation but also for portfolio resilience in the face of systemic volatility.

Beyond the Primary Market Bias

Institutional real estate investing has traditionally coalesced around primary markets—large, globalized cities perceived to offer liquidity, scale, and economic diversity. Yet in the wake of sustained disruptions (the 2008–2009 global financial crisis, the COVID-19 pandemic, and a historic rate-hike cycle), this thesis warrants reexamination. To assess how smaller geographies perform across economic and market cycles, Graceada Partners conducted longitudinal research across 12 secondary and tertiary Western US markets: the California cities of Bakersfield, Fresno, Modesto, Sacramento, and Stockton; the Colorado cities of Colorado Springs, Denver, and Fort Collins; the Utah cities of Ogden, Provo, and Salt Lake City; and Reno, NV. These cities were selected because of not only Graceada’s investment footprint but also their representative qualities in reflecting the broader performance of secondary and tertiary metros in the region. The findings, drawn from Oxford Economics, the Bureau of Economic Analysis, CoStar, and proprietary analysis, paint a sharply different picture from conventional assumptions about the relative risk and return of smaller markets. The comprehensiveness and consistency of the data across two decades indicate that these markets, far from being niche or peripheral, should be central to the conversation around durable, yield-generating real estate strategies.

The purpose of this article is to present a data-grounded reexamination of outdated investment heuristics that reflexively favor primary markets. We aim to provide institutional investors with a framework to better understand and evaluate the evolving performance dynamics of smaller Western US cities—and why, in today’s climate, those dynamics may be better aligned with riskadjusted return goals than the traditional gateway cities.

Economic Resilience: Measuring Vibrancy Across Market Cycles

Contrary to perception, secondary and tertiary markets demonstrate stronger long-term economic and population growth, more consistent job creation, and lower volatility in income and employment metrics than primary markets (Exhibit 1). Between 2002 and 2022, GDP growth in secondary and tertiary markets averaged 5.05%—36 basis points (bps) higher than in Western US primary markets. During the financial crisis, GDP growth in secondary and tertiary markets outperformed primary markets by 300 bps. During the COVID-19 pandemic, a similar pattern emerged. While primary markets had 0.00% GDP growth, smaller markets continued to expand at a moderate and consistent pace of 1.43%. This resilience is not a temporary phenomenon but a consistent structural feature of these geographies, rooted in broader-based economies, more affordable cost structures, and population trends that support organic demand.

The broad takeaway is that smaller markets not only deliver growth but do so with a more predictable trajectory than primary markets. This dynamic has significant implications for underwriting and portfolio stability, especially in environments characterized by rising interest rates and tightening liquidity. From an institutional risk management perspective, consistent economic indicators such as these can create a more predictable cash flow base—particularly important for core-plus and long-duration capital strategies.

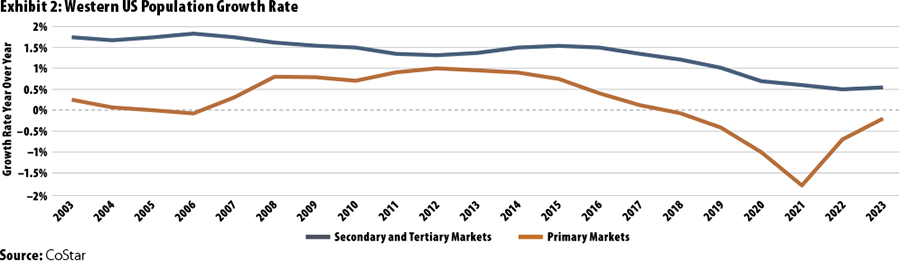

In addition to headline economic growth, an analysis of volatility in these indicators reveals that secondary and tertiary markets are not only more robust but also more predictable. For instance, population growth in these markets has been consistently positive and exhibited significantly less year-over-year variability than in primary markets (Exhibit 2). And there was no post-pandemic "bump" in population growth but rather consistent year-over-year growth. This demographic stability contributes to more reliable demand for residential and industrial space.

Unemployment metrics further support this narrative. Over the past two decades, secondary and tertiary markets have averaged 6.04% unemployment compared with 6.39% in primary markets, with lower peaks during economic contractions. Notably, during both the financial crisis and the pandemic, smaller markets experienced less severe labor dislocation. These factors collectively point to stronger economic underpinnings and a more durable base for real estate demand than typically assumed.

Taken together, the findings challenge the heuristic that size and scale automatically confer economic resilience. Instead, the data reveal that right-sized economies with diverse industry bases, demographic momentum, and policy stability may offer a more compelling risk-return profile—especially in a macro environment in which volatility is likely to remain elevated.

Dispelling the "One-Mill Town" Myth: Economic and Demographic Depth

Perhaps one of the less recognized characteristics of secondary and tertiary markets in the Western US is their degree of economic diversity. In ten of the 12 cities analyzed, no single industry accounted for more than 17% of GDP. Sacramento and Colorado Springs were exceptions, where the government sector accounted for just above 20%. In stark contrast, more than 50% of San Francisco Bay Area GDP is dependent on the tech sector. Unlike the quintessential "onemill town" that may be envisioned with the phrase "secondary and tertiary markets," these are cities with metropolitan statistical area populations of half a million to three million and large, diversified economies.

The diversity of industry participation across these markets is a key differentiator. For instance, Fresno’s GDP is distributed across sectors such as agriculture, education, health care, real estate, manufacturing, and logistics, with each contributing significantly but none dominating the local economy (Exhibit 3). This structural balance helps mitigate exposure to single-industry downturns, in contrast to tech-centric metros such as San Francisco, where a cyclical correction in technology reverberates broadly across commercial real estate performance.

This diversification also manifests in employment data. During the financial crisis, Fresno, Reno, and Provo had more moderate rises in unemployment than primary markets because of the buffering effect of varied economic drivers. More recently, during the pandemic, markets such as Ogden and Fort Collins quickly rebounded in job creation, thanks in part to local resilience in education, health care, and logistics. These examples underscore that diversity is not just theoretical but observable in market outcomes.

Another overlooked dimension of economic resilience is labor force participation and labor mobility. Secondary and tertiary markets often have a greater share of working-age populations as a proportion of total population and a lower average age. These factors, combined with cost-of-living advantages, support the retention and attraction of upwardly mobile talent.

Real Estate Fundamentals: Risk-Adjusted Outperformance

Economic vibrancy translates into tangible real estate performance. Across both workforce housing and industrial sectors, secondary and tertiary markets exhibit consistently strong and more stable fundamentals. Rent growth, net absorption, and valuation trends indicate these markets are not only viable but competitive.

In secondary and tertiary markets, workforce housing

◼ had rent growth of 3.02% annually versus 2.58% in primary markets

◼ showed net absorption of 0.73% annually, more than double the 0.33% in primary markets

◼ exhibited cap rates higher than in primary markets by about 45 bps, though they have been converging since 2008

◼ showed price appreciation since 2016 that has been stronger than in primary markets

In secondary and tertiary markets, industrial

◼ showed net absorption of 1.59% versus –0.03% in primary markets

◼ had rent growth that outperformed during the financial crisis and since 2018, though primary markets led on a 20-year basis

◼ experienced vacancy rates during the financial crisis equivalent to (not greater than) in primary markets

◼ exhibited cap rates about 160 bps higher than in primary markets, offering potential for cap rate convergence (and compression) over time

These data points support the case for underwriting with more confidence. Higher cap rates in secondary and tertiary markets offer enhanced entry yields, while evidence of convergence in some sectors (notably multifamily) suggests long-term upside as these markets continue to institutionalize (Exhibit 4). Lower volatility in fundamentals further reinforces the suitability of these markets for stable, income-generating strategies.

Additionally, the relatively smaller scale of assets in these markets allows institutional investors to enter at favorable price points, build scale over time, and still achieve meaningful diversification within a single metro while maintaining liquidity (Exhibits 5 and 6). This strategy also allows for deeper market knowledge and operational efficiency, key differentiators in generating outperformance in less crowded markets.

More Stable Supply-and-Demand Dynamics

One of the most interesting observations from our research was that secondary and tertiary markets in the Western US exhibit higher net absorption and lower volatility in net absorption—meaning demand is stronger and these markets are less subject to the "boom-bust" development cycle and oversupply risk than their primary market counterparts (Exhibit 7).

This runs counter to the prevailing sentiment that ample undeveloped land is the greatest determinant of oversupply risk. Rather, the presence of institutional capital is a greater indicator of oversupply risk—primary markets show more volatility in net absorption and lower overall net absorption. Even within the secondary and tertiary market dataset, markets that have greater institutional favorability (e.g., Denver and Salt Lake City) experienced increased oversupply versus markets such as Bakersfield and Fort Collins.

This divergence in capital allocation behavior—in which primary markets attract more speculative capital during up cycles—tends to exacerbate downside risk when cycles turn. In contrast, development activity in secondary and tertiary markets tends to be more demand driven and often funded by local or regional capital sources that adhere to tighter underwriting standards. This structural conservatism acts as a moderating force and enables smaller markets to maintain better equilibrium in real estate markets.

This demand-driven development model produces healthier fundamentals over time and translates to lower rent growth volatility, particularly notable in multifamily (Exhibit 8). These dynamics support both income stability and long-term appreciation.

Why Secondary Markets Often Outperform During Downturns

The comparative stability of these markets stems from structural factors: limited speculative development, conservative capital deployment, and less dependence on global capital flows. During the global financial crisis, for instance, both multifamily and industrial vacancy rates in secondary and tertiary markets increased at similar or smaller magnitudes than in primary markets, despite lower initial absorption rates. This pattern of resilience is not anecdotal but consistent across downturns. For example, during the financial crisis, while gateway markets experienced significant declines in multifamily occupancy, cities such as Provo and Colorado Springs maintained occupancy rates within 100 bps–150 bps of precrisis levels.

In workforce housing, rent declines during downturns were milder and recoveries faster in these markets. Since 2016, valuation growth in secondary and tertiary multifamily properties outpaced that of primary markets, even through the rate-hike period. This implies that investor capital has started to recognize the embedded stability and income durability of these locations.

From a portfolio construction standpoint, incorporating secondary and tertiary markets provides an effective counterbalance to assets in more cyclical, globally integrated cities. These markets not only show more favorable long-term trends but also exhibit more muted drawdowns in economic and real estate performance during downturns, characteristics that align well with the growing institutional focus on capital preservation and downside protection.

Conclusion: From Outlier to Opportunity Set

The current phase of institutional strategy evolution echoes prior frontier expansions, such as into student housing, self-storage, and manufactured housing. Each faced initial skepticism because of perceived operational complexity or "noninstitutional" status. Yet early adopters in those sectors captured superior returns and benefited from lower competition.

Secondary and tertiary geographies now represent a parallel moment in the institutional real estate evolution. Factors such as pricing dislocation, demographic shifts, and post-pandemic behavioral changes have created a convergence of incentives to consider markets that were once viewed as peripheral. These cities offer not just favorable entry points but access to younger populations, diversified employment centers, a more favorable regulatory climate, and embedded resilience through long-term population growth.

As volatility persists and macroeconomic uncertainty deepens, geographic diversification remains a powerful risk mitigant. The evidence presented here underscores that secondary and tertiary Western US markets are not merely acceptable substitutes for primary markets— they are, in many cases, structurally advantaged. Their performance across economic and real estate metrics reveals a mismatch between institutional perception and reality.

The continued underrepresentation of these markets in institutional portfolios presents a rare asymmetry: a class of geographies that has delivered above-average returns with below-average volatility yet remains discounted by legacy allocation models. As capital markets evolve and investors seek better alignment with demographic and economic mega trends, this asymmetry is unlikely to persist. Institutions willing to challenge convention and embrace a broader geographic lens are well positioned to capture not only incremental returns but greater portfolio durability in a changing economic era.

This article has been prepared solely for informational purposes and is not to be construed as investment advice or an offer or a solicitation for the purchase or sale of any financial instrument, property, or investment. It is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. The information contained herein reflects the views of the author(s) at the time the article was prepared and will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing or changes occurring after the date the article was prepared.